The worldwide mobile phone market is forecast to grow 7.3% year over year in 2013, marking a sharp rebound from the nearly flat (1.2%) growth experienced in 2012. Strong demand for smartphones across all geographies will drive much of this growth as worldwide smartphone shipments are expected to surpass one billion units for the first time in a single year, according to the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker.

The overall mobile phone market is growing faster than previously forecast thanks to a stronger-than-expected first half of the year driven by strong gains in emerging markets and the sub-$200 smartphone segment. IDC previously projected 5.8% growth for the year. Vendors are now forecast to ship more than 1.8 billion mobile phones this year, growing to over 2.3 billion mobile phones in 2017.

The overall mobile phone market is growing faster than previously forecast thanks to a stronger-than-expected first half of the year driven by strong gains in emerging markets and the sub-$200 smartphone segment. IDC previously projected 5.8% growth for the year. Vendors are now forecast to ship more than 1.8 billion mobile phones this year, growing to over 2.3 billion mobile phones in 2017.

Worldwide smartphone shipments are forecast to grow 40.0% year over year to more than 1.0 billion units this year. High smartphone growth is the result of a variety of factors, including steep device subsidies from carriers, especially in mature economic markets, as well as a growing array of sub-$200 smartphones. Total smartphone shipments are forecast to reach 1.7 billion units in 2017.

“Two years ago, the worldwide smartphone market flirted with shipping half a billion units for the first time – to double that in just two years highlights the ubiquity that smartphones have achieved,” said Ramon Llamas, Research Manager with IDC’s Mobile Phone team. “The smartphone has gone from being a cutting-edge communications tool to becoming an essential component in the everyday lives of billions of consumers.”

“Smartphones will represent virtually all of the mobile phone market in many of the world’s most developed economies by the end of 2017,” said Kevin Restivo, Senior Research Analyst with IDC’s Worldwide Mobile Phone Tracker program. “Aggressive carrier subsidies of handsets, falling prices, higher consumer awareness, and a vast array of devices will mean almost all phones shipped to the developed world will be ‘smart.’ However, smartphone shipment volume will be dominated by emerging markets, such as China, even though the percentage of smartphones to feature phones won’t be as high.”

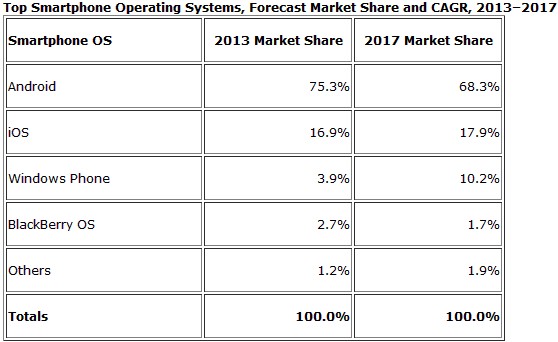

Smartphone Operating Systems

“Underpinning the smartphone market is an evolving market for operating systems,” added Llamas. “We believe Android and iOS will remain the clear number one and two platforms, respectively, throughout our forecast. What remains to be seen is how Windows Phone and BlackBerry’s respective futures will play out pending their recent announcements. Windows Phone has inched ahead of BlackBerry during the first half of 2013, and we believe that will extend into the future. However, overall shipments will continue to trail those of Android and iOS.”

Android remains the dominant smartphone operating system, a status that won’t change even though its share will decline somewhat as the market matures and competition solidifies. The sheer volume of devices at a wide range of price points combined with Google’s backing and a growing application library will keep Android atop the smartphone O.S. heap. Samsung remains the world’s top seller of Android-based smartphones, while the resurgence of LG and Sony have also contributed to its success in recent quarters.

iOS will remain the clear number two operating system as the expected launch of a lower-cost iPhone will open up a wider addressable market. Apple will also grow faster in subsequent forecast years due to enterprise and emerging market share gains that will be driven in part by a likely deal with China Mobile, which will give it greater reach into one of the world’s fastest-growing smartphone markets. iOS share gains will be tempered by the relatively high price points of the iPhone, which makes for a lower share ceiling.

Windows Phone will solidify its position as the number three O.S. with incremental share gains over the course of the forecast. With the acquisition of Nokia’s device and services unit, Microsoft will increasingly need to drive share gains by itself as OEM support for Windows Phone is expected to wane now that the company is set to become a full-fledged hardware maker. Microsoft will also need to ship more low-cost smartphones to high-growth emerging markets if it is to continue building on its recent nominal share increases.

BlackBerry OS share will decline markedly over the forecast due to tepid BlackBerry 10 reception and emboldened competition that are expected to whittle away share in its remaining regional bastions of strength, such as Africa, Latin America, and the Middle East. BlackBerry volume will remain flat as the market expands around it thanks to enterprises with security or other specialized needs that continue to purchase devices from the company.